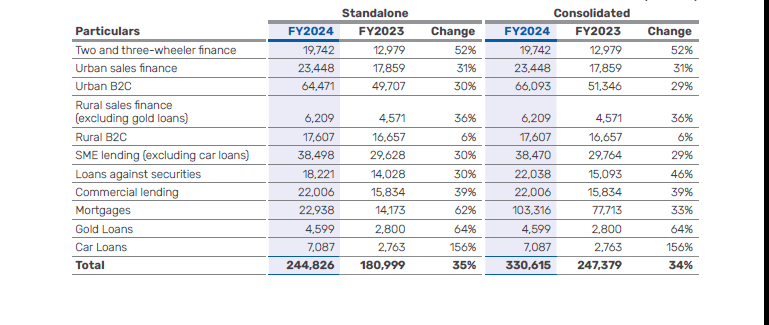

Bajaj Finance has built a strong business with a diversified portfolio in the Indian economy. It manages an Assets Under Management (AUM) of nearly ₹3,50,000 crores and continues to show robust growth, having recorded approximately 34% growth in FY2024, reaching an AUM of ₹3,30,615 crores. The company has established a strong presence in both rural and urban markets, contributing to commendable and sustainable growth.

When we talk about Bajaj Finance business model, several segments stand out. These include financing for two-wheelers and three-wheelers, urban sales finance, SME lending, rural B2C, commercial lending, cross-sell businesses, car loans, and gold loans. The company’s presence across these segments is driving significant AUM growth.

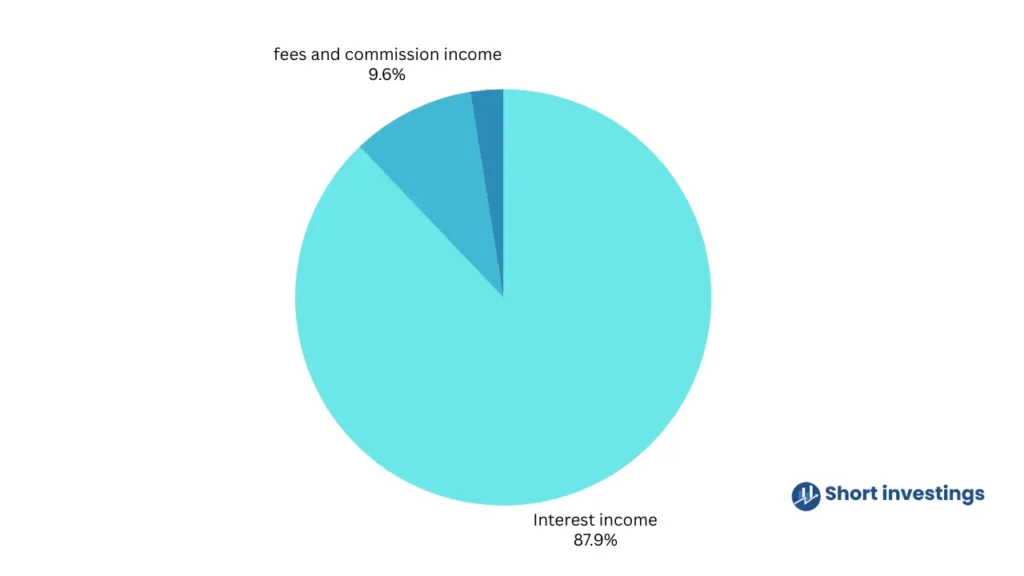

How Bajaj finance revenue generated

Bajaj Finance is one of the leading NBFCs (Non-Banking Financial Companies) in India. Like most NBFCs, its primary source of revenue is interest income. Simply put, when a customer purchases a product on EMI or takes a loan from Bajaj Finance, the company charges interest on that amount. This interest paid by the customer becomes one of the key and largest sources of revenue for the company.

It operates a business model similar to that of its banking peers, such as HDFC Bank and ICICI Bank.

The company previously generated approximately ₹54,982 crores in revenue. One of the major sources of this revenue was interest income, which amounted to ₹48,306.60 crores. The second largest contributor was fees and commission income, totaling ₹5,267.17 crores. This highlights that interest income remains the primary source of revenue for the company.

If we dive deeper into how Bajaj Finance lends money, we find that Urban Sales Finance holds a portfolio of nearly ₹23,000 crores. In the Urban B2C (Business to Consumer) segment, the portfolio stands at approximately ₹66,093 crores. One of the biggest contributors to its lending business is the mortgage segment, with a portfolio size of ₹1,03,316 crores. This highlights Bajaj Finance’s continued focus on building revenue through these key areas.

Additionally, there are several other segments showing significant growth. For instance, gold loans witnessed a remarkable 64% growth in revenue. Similarly, the 2-wheeler and 3-wheeler finance segments recorded a 52% growth, making them two of the fastest-growing areas for the company.

Overall, if the broader economy sees continued growth in mortgages, 2-wheeler and 3-wheeler financing, and Urban B2C lending, Bajaj Finance is likely to benefit significantly. On the other hand, even if gold loan growth remains strong, its impact may be limited compared to the influence of mortgage growth in Bajaj Finance’s overall business scenario.

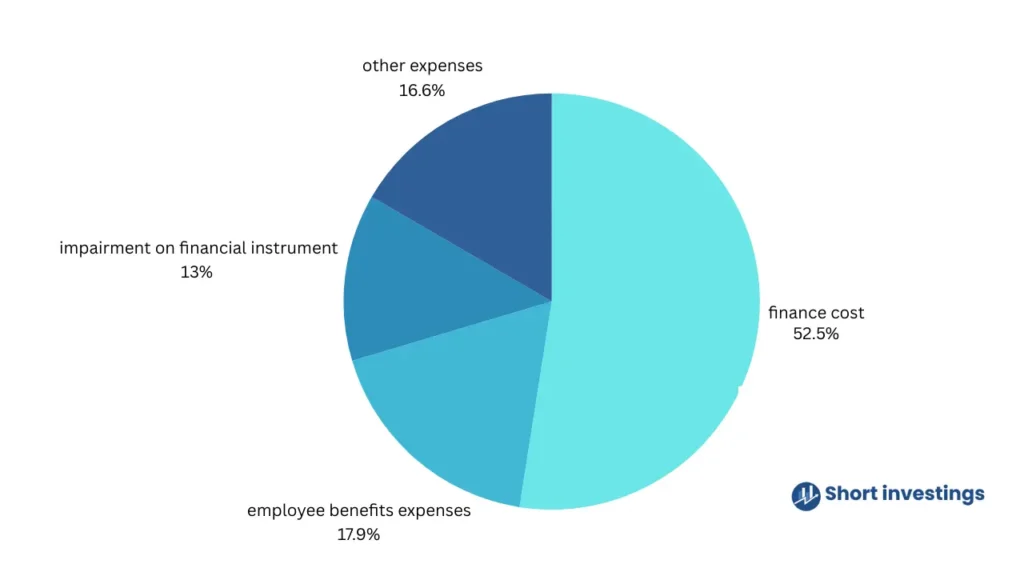

Expenses of Bajaj Finance

As discussed in Bajaj Finance’s business model, the company lends money to consumers. To do this, it requires capital, which it raises through various means—primarily by accepting public deposits such as Fixed Deposits (FDs). The company holds a public deposit portfolio of around ₹38,000 crores and has raised an additional ₹22,000 crores through other sources, bringing the total deposits to approximately ₹60,000 crores.

Bajaj Finance earns interest income from consumers who borrow money. However, it also needs to pay interest to those who have provided deposits. This interest payout represents the finance cost, which is one of the company’s major expenses. In FY2024, the finance cost amounted to approximately ₹18,724 crores.

Other key expenses include:

Fees and commission expenses: ₹1,931.50 crores

Employee benefit expenses: ₹6,396.01 crores

Other operating expenses: ₹3,014.36 crores

These costs are essential for the functioning of the company and form a significant part of its overall expenditure.

Bajaj Finance Omni-Channel Strategy

Bajaj Finance follows an omni-channel strategy. In this strategy, the company connects with customers through multiple platforms—whether it’s online or offline—and provides a seamless experience. The company offers its services through mobile apps, websites, and also through offline stores. This helps customers connect with Bajaj Finance easily, whether they are using a digital platform or visiting a physical store.

This strategy helps the company reach more people, improve customer service, and make the process of taking loans or using other financial services simple and quick. Through this, Bajaj Finance is trying to create a strong connection with customers across all platforms.

Bajaj Finance Business Sustainability & future perspective

Bajaj Finance is experiencing nearly 20% growth every month, which, as the management has mentioned, is due to a strong strategy—especially its omni-channel strategy—that is delivering long-term benefits.

The company also has one of the highest product-per-customer (PPC) ratios. This simply means how many times a customer has availed services or taken loans from the same company. In this case, Bajaj Finance stands out as it reflects how often consumers return to take loans or use services again from the company. This is a highly relevant and convenient factor contributing to the sustainability of Bajaj Finance’s business.

Currently, the company has a PPC of around 6.15, which means a single customer, on average, has availed services from Bajaj Finance six times. This shows how effective and convenient their business model is, and how strong their customer retention efforts are.

It’s not just about expanding into new areas or acquiring more customers from rural and urban regions—though the company is definitely making efforts in that direction as well. What’s equally important is how they are maximizing value from their existing customer base. This approach adds significantly to the sustainability and growth of Bajaj Finance.

This is why the company is achieving more than 25% year-on-year growth. They also offer products through different subsidiaries, such as Bajaj Housing Finance Limited (BHFL) and Bajaj Finance Securities Limited. These subsidiaries help Bajaj Finance offer more diverse services, making it more convenient for customers and increasing the company’s overall reach.

As the company continues to experience sustainable growth in both rural and urban areas, the sector is becoming more convenient through digitalization. Bajaj Finance is also working on implementing AI models and other technologies to reduce operational costs.

Several internal developments are taking place within the company, and it has also established a strong partnership with Airtel to offer services through its application. In addition, the company has formed several other partnerships, which are enhancing the future prospects of the Bajaj Finance business model and paving the way for even greater growth and expansion.

factor which might cause the Bajaj finance business model

The key consideration in Bajaj Finance’s business model is that the company earns the majority of its revenue from interest income. So, if there is any increase in the cost of borrowing, it becomes a negative factor for the company’s margins.

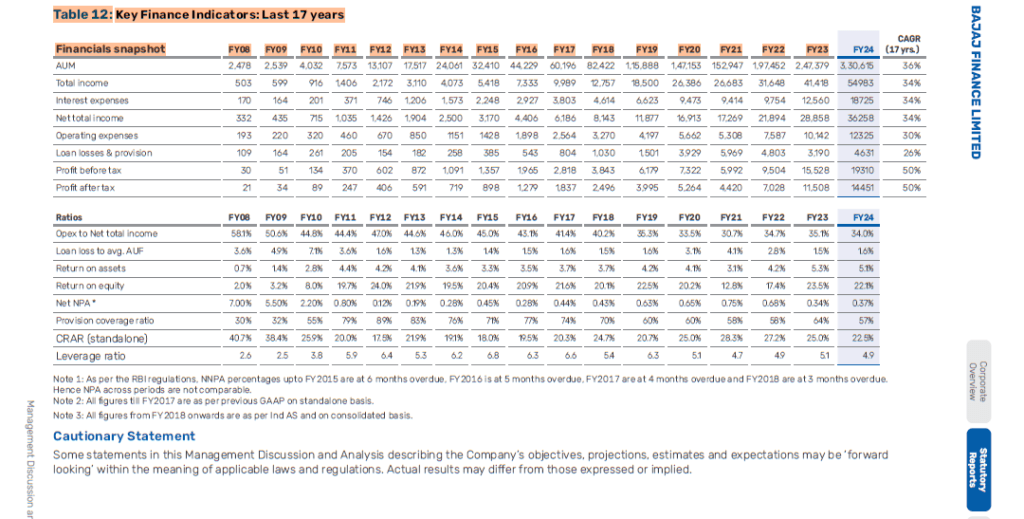

A similar situation occurred previously. In the financial year 2020, the company’s operating expenses to net interest income ratio was around 33.5%, and in financial year 2024, it has risen slightly to 34%. This slight increase is a negative sign because if the company’s margins are not improving, it’s not a good thing. Ideally, operating expenses should be lower in comparison to net interest income. The lower this ratio gets, the better it is for the company.

One more point is that this rise in expenses also happened because the company had earlier focused more on unsecured loans instead of secured ones. However, after RBI’s tightening stance, the company started focusing more on secured loans. As seen in the above section, the company has shown major growth in revenue and AUM from the mortgage segment, which is a secured form of lending.

Another important factor is high inflation, which may push monetary policy towards a contractionary stance. That would be unfavorable for the company, because if interest rates rise, the cost of borrowing for Bajaj Finance will also increase. This, in turn, would have a negative impact on the company’s business.

3 thoughts on “Bajaj finance business model; Revenue of Bajaj finance, expenses, Omnichannel strategy and more”