Kaynes Technology India stock has fallen more than 18%, and the futures are indicating a further decline of nearly 20%. The market has been disappointed not only because of the quarterly results, but also because of the commentary made by the CFO in the last quarter. In fact, the market reaction appears to be more negative toward the management commentary than the actual results themselves.

In the third quarter of FY2026, Kaynes Technology India delivered results that did not meet market expectations. The company had highlighted concerns regarding several orders and executions that were still pending, due to which those numbers were not reflected in the balance sheet.

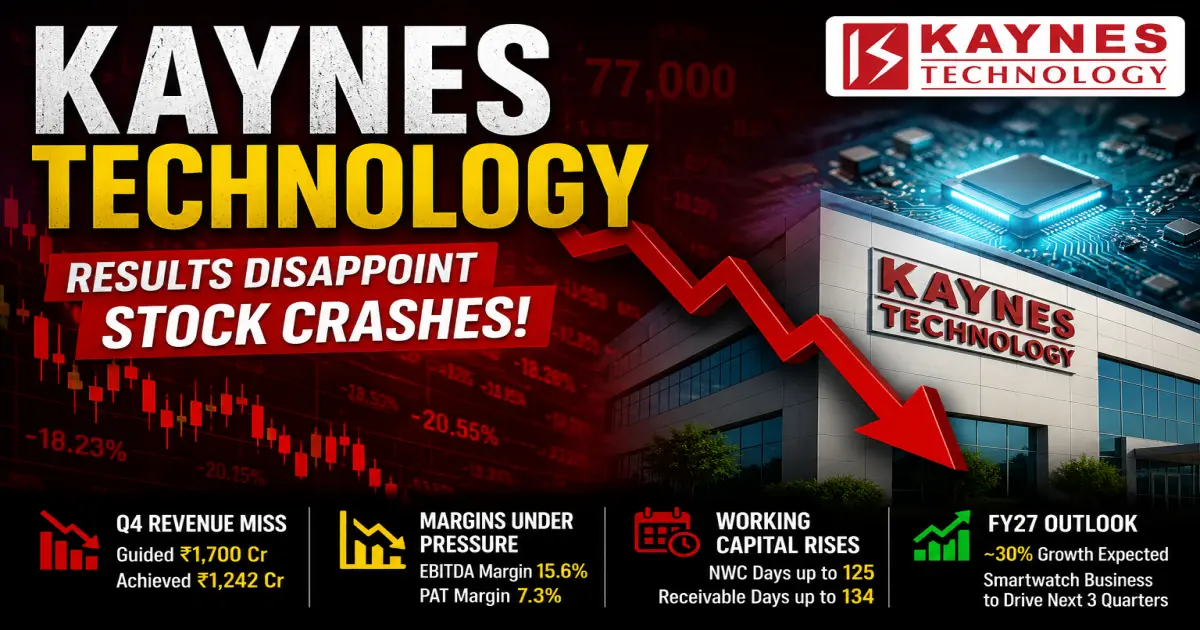

Following this, Kaynes CFO Jayaram Sampath confidently stated that the company would achieve revenue of ₹1,700 crore in Q4. However, the company unexpectedly reported revenue of only around ₹1,200 crore in Q4, which became a major concern for brokers, retailers, and the overall market, as the actual performance was far below management guidance.

Earlier as well, the management had faced allegations regarding irregularities in accounting policies, as highlighted in a report published by Kotak institutional. Following those concerns, the stock had already witnessed a sharp correction from its higher levels.

Kaynes Technology India has continued to deliver strong revenue growth, with sales rising nearly 33% in FY26 to around ₹3,626 crore. However, compared to the previous few years, the growth rate has slightly slowed down. Earlier, the company was consistently reporting growth of around 50–60%, which had created very high expectations in the market. So, even though 33% growth is still strong on an absolute basis, investors were disappointed because the growth momentum slowed compared to earlier years.

At the same time, profitability also came under pressure. The EBITDA margin declined to around 15.6%, while the PAT margin dropped sharply to nearly 7.3%. This indicates that despite higher revenue, the company was unable to convert that growth efficiently into profits. Rising finance costs, execution delays, and higher operating expenses impacted the overall profitability during the quarter.

Another major concern came from the working capital side. Net working capital days increased from 87 days in FY25 to 125 days in FY26, which means more cash is getting stuck in the business for a longer period. Receivable days also jumped significantly from 84 to 134 days, showing that the company is taking much more time to collect payments from customers.

Inventory days increased as well, meaning inventory remained unsold for a longer duration, while payable days also rose. Altogether, these numbers suggest that cash flow efficiency weakened during the year. This is one of the key reasons why the market reacted negatively, because investors generally expect a fast-growing company to maintain strong execution, healthy cash flow, and stable margins alongside revenue growth.

Despite the weak quarterly performance, Kaynes Technology India management remains confident about the future growth outlook. The company is expecting nearly 30% revenue growth in the next financial year, which continues to reflect strong long-term business potential.

During the concall, the management also highlighted that the smartwatch segment is expected to contribute meaningful revenue over the next three quarters. This gives additional strength to the company’s business outlook, as newer segments are gradually scaling up alongside its core EMS business.

Overall, while the recent results and margins disappointed the market in the short term, the company still expects healthy growth going forward, supported by increasing demand, business expansion, and new revenue opportunities.

Why did Kaynes Technology India stock fall sharply?

The main reason behind the sharp fall in the stock was the disappointing quarterly performance and the gap between management guidance and actual execution. Earlier, the company management had guided for nearly ₹1,700 crore revenue in Q4, but the company reported only around ₹1,243 crore revenue. This significantly disappointed investors and brokers because market expectations were built around the management’s earlier commentary.

Apart from this, weaker margins, rising finance costs, and increasing working capital pressure also created concerns regarding execution efficiency and cash flow management.

What is the expected growth outlook for FY27?

The company management has guided for nearly 30% growth in the coming financial year, which still reflects strong long-term business potential. Despite short-term weakness, the management remains confident about demand across multiple segments and expects business momentum to improve gradually.

The company believes that execution improvement and stronger order conversion may support future growth over the next few quarters.

Why is the market concerned about margins and profitability?

Although the company reported strong sales growth, profitability weakened during the quarter. EBITDA margin declined to around 15.6%, while PAT margin fell sharply to nearly 7.3%.

This indicates that the company faced pressure from higher costs, slower execution, and increased finance expenses. Investors generally expect high-growth companies to maintain strong margins, so the decline in profitability negatively impacted market sentiment.