Persistent Systems is emerging as one of the fastest-growing IT companies in India. The company has built a strong position in digital engineering, cloud computing, AI solutions, software modernization, and enterprise transformation services. While many traditional IT companies are currently witnessing slower growth, Persistent Systems continues to maintain strong double-digit growth along with improving profitability.

One of the most important things about the company is that it is heavily focused on future technologies such as Artificial Intelligence, cloud platforms, data engineering, and digital transformation. Along with this, the company has also built strategic partnerships with global technology leaders like NVIDIA and Databricks, which is strengthening its long-term business opportunities.

In this blog, we will understand the business model of Persistent Systems, its revenue mix, geographical presence, client stability, financial performance, partnerships, and valuation.

Understanding the Business of Persistent Systems

Persistent Systems mainly makes money by providing digital engineering, cloud, AI, software development, and platform modernization services to global enterprises. The company helps businesses modernize their technology infrastructure, improve operational efficiency, manage enterprise data, and build AI-powered platforms.

The company operates across three major business segments:

- Software, Hi-Tech & Emerging Industries

- Banking, Financial Services & Insurance (BFSI)

- Healthcare & Life Sciences

These three segments together drive the company’s overall revenue growth.

Segment-Wise Revenue Analysis

1. Software, Hi-Tech & Emerging Industries

This is the largest business segment for Persistent Systems. In FY26, the segment contributed around 39.8% of the total revenue, while in Q4FY26 the contribution stood at around 39.2%.

The segment generated nearly $170.8 million revenue in Q4FY26 with around 11.2% YoY growth. Under this segment, the company mainly works with technology companies, telecom businesses, and emerging digital industries.

Persistent Systems helps these companies shift from hardware-focused systems toward software-led platforms. The company also works on cloud modernization, AI-enabled systems, digital infrastructure, and enterprise engineering solutions.

2. Banking, Financial Services & Insurance (BFSI)

The BFSI segment contributed around 34.6% of FY26 revenue and around 34.5% in Q4FY26.

This segment generated nearly $150.4 million revenue in Q4FY26 with around 24.3% YoY growth, making it one of the fastest-growing business segments for the company.

Under this division, Persistent Systems works on payment modernization, underwriting platforms, workflow automation, digital banking infrastructure, and enterprise financial platforms for banks and insurance companies.

The strong growth in this segment indicates rising demand for digital transformation and AI-based financial solutions globally.

3. Healthcare & Life Sciences

The Healthcare & Life Sciences segment contributed around 25.6% of FY26 revenue and around 26.3% in Q4FY26.

The segment generated nearly $114.8 million revenue in Q4FY26 with around 14.1% YoY growth.

In this segment, Persistent Systems provides digital healthcare transformation services, analytics systems, care management platforms, cloud infrastructure, and operational efficiency solutions for healthcare and life science companies.

The business is benefiting from increasing global adoption of digital healthcare and AI-based healthcare systems.

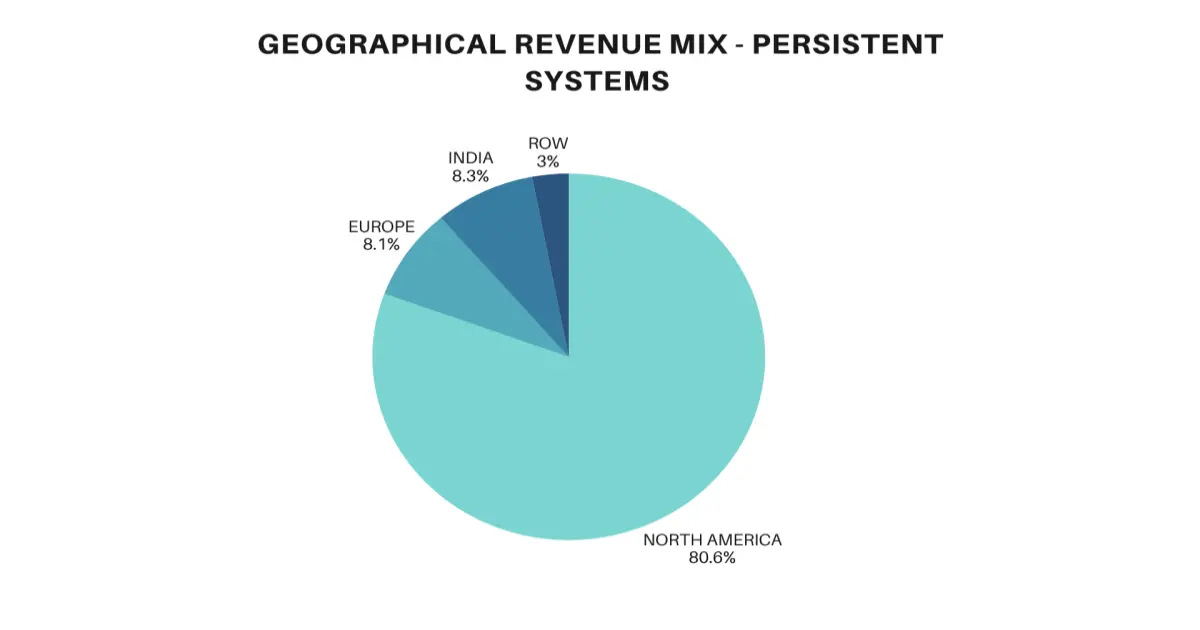

Geographical Revenue Mix

One of the most important things to understand about Persistent Systems is its geographical revenue mix.

According to FY26 data, nearly 80.6% of the company’s revenue comes from North America, while India contributes only around 8.8%.

In Q4FY26 specifically, North America alone contributed around 81.4% of the total revenue, whereas India contributed only around 8.3%.

This clearly shows that Persistent Systems is heavily dependent on the US market for its revenue growth.

The importance of the American market is very high because the company earns the majority of its revenue in US dollars. If enterprise technology spending in the US remains strong, Persistent Systems can continue benefiting from increasing demand for AI, cloud, digital engineering, and enterprise transformation services.

At the same time, any slowdown in US technology spending can also impact the company because of its heavy dependency on the North American market.

Strategic AI Partnerships

Another major strength of Persistent Systems is its strategic partnerships with global technology leaders like NVIDIA and Databricks.

The company partnered with NVIDIA to launch AI-powered generative molecules and virtual screening solutions for healthcare and life sciences businesses. Through NVIDIA’s AI platform, Persistent Systems is helping pharma and biotech companies improve molecular simulation and drug discovery processes.

At the same time, the company partnered with Databricks to launch a merchant risk management solution powered by Databricks AI. This solution helps financial institutions and payment companies improve fraud detection, risk analysis, compliance monitoring, and real-time decision-making.

These partnerships are important because they show that Persistent Systems is expanding beyond traditional IT services and building strong capabilities in AI, cloud computing, data engineering, and enterprise AI solutions.

Hedging Strategy and Revenue Stability

Persistent Systems also actively hedges its contracts to reduce currency-related risks.

In Q4FY26, the company reported around $500 million in outstanding hedges at a hedge rate of nearly ₹90.7 per dollar.

This is important because most of the company’s revenue comes from the US market and is earned in US dollars rather than Indian rupees.

Through hedging, the company tries to protect its future revenues from sudden currency fluctuations. At the same time, depreciation in the Indian rupee also benefits the company because dollar-denominated revenues translate into higher rupee earnings.

Revenue Concentration and Client Stability

The revenue concentration data also reflects strong business stability.

In FY26:

- Top 5 clients contributed around 32.2% of revenue

- Top 10 clients contributed around 41.6%

- Top 20 clients contributed around 52.9%

These numbers have remained relatively stable over the past several quarters, which indicates that the company has strong long-term relationships with its major clients.

The client engagement data also shows stable business execution.

In FY26, the company had:

- 4 clients contributing more than $75 million annually

- 8 clients in the $20 million to $50 million category

- 17 clients in the $10 million to $20 million category

One important observation is that during the last four quarters, the company has not added many new ultra-large clients above the $50 million category. However, the increase in the $20 million to $50 million category from 6 to 8 clients indicates improving engagement with mid-to-large enterprise customers.

Quarterly Financial Performance: Q4FY26 vs Q4FY25

Persistent Systems delivered strong financial growth in Q4FY26.

The company reported revenue of around $436 million, which increased by nearly 16.2% YoY compared to Q4FY25.

At the same time, total direct costs also increased by around 24.3%, showing that the company is continuously investing in employees, delivery capabilities, and business expansion.

Despite rising costs, the company managed to improve profitability strongly.

- Gross Profit increased by around 26.6% YoY

- EBITDA increased by around 31.4% YoY to ₹7,677 million

This is an important highlight because many large IT companies are currently witnessing slower growth rates, while Persistent Systems continues to maintain strong double-digit growth along with improving margins.

Full-Year Financial Performance: FY26 vs FY25

On a full-year basis, Persistent Systems also delivered strong performance.

- Revenue increased by around 17.4% YoY to nearly $1.65 billion

- Gross Profit increased by around 27.2%

- EBITDA increased by around 31.5%

These numbers indicate that the company is not only growing its revenue strongly but is also improving operational efficiency and profitability.

Persistent Systems currently trades at a significantly higher valuation compared to many traditional IT companies.

The company’s P/E ratio is around 41.76, whereas Infosys trades near 15.90.

At first glance, this may appear expensive, but the reason behind the premium valuation is the company’s strong growth rate.

Over the last three years:

- Persistent Systems delivered around 20.88% sales growth

- Infosys delivered around 6.77% sales growth

This means Persistent Systems is growing at more than double the pace of Infosys.

Because of this strong growth momentum, improving profitability, AI-focused partnerships, and exposure to future technologies, investors are willing to assign a premium valuation to the company.

Conclusion

Overall, Persistent Systems appears to be one of the strongest high-growth companies in the Indian IT sector.

The company has built a diversified business across Software, BFSI, and Healthcare segments while maintaining strong client relationships and improving profitability.

Its strategic partnerships with NVIDIA and Databricks are helping the company strengthen its position in AI, cloud computing, and enterprise digital transformation.

Along with this, the company continues to maintain strong revenue growth compared to many traditional IT companies.

Although the valuation remains premium, the market is justifying this valuation because of Persistent Systems’ faster growth rate, AI-driven opportunities, strong execution, and improving financial performance.

Going forward, the company’s ability to maintain high growth in the US market, expand large client relationships, and capitalize on AI opportunities will remain key factors for future growth.