The recent numbers and business highlights give a clearer picture of how Netweb Technologies is evolving beyond just a traditional IT hardware player.

The company reported revenue of ₹11,490.2 million with a strong 58.7% year-on-year growth, which signals that demand is not only present but accelerating. What stands out to me is the balance in its customer base—almost evenly split between government (50.6%) and non-government (49.4%). This reduces dependency risk and shows that the company is able to execute across both institutional and enterprise segments.

On the policy support side, receiving ₹59.4 million under the PLI scheme is an important tailwind. It directly supports manufacturing and scale, which can further strengthen margins and competitiveness over time. It also reflects that the company is aligned with government priorities in electronics and telecom infrastructure.

From a business perspective, the client base is quite diversified. The company is working with government bodies, defence institutions, BFSI players, educational institutions, and large enterprises including IT, telecom, and cloud segments. This kind of multi-sector presence indicates that its offerings—especially in high-performance computing and AI infrastructure—are finding relevance across industries, not just in niche areas.

What makes the story more interesting is the shift towards AI and advanced computing. With AI becoming a meaningful revenue contributor and strong collaboration with NVIDIA, the company is positioning itself in a high-growth segment. This is not just about selling hardware anymore—it’s about building integrated AI and cloud ecosystems.

How the Netweb does business

Netweb’s core strength clearly comes from its high-performance computing (HPC) business, and this is where the foundation of its growth is being built. The company is not just supplying systems—it is designing and deploying supercomputing solutions that are already being used by some of India’s most advanced research and institutional setups. Systems like AIRAWAT, PARAM Yuva-II, and others show that the company is operating in a space that requires both technical depth and execution capability.

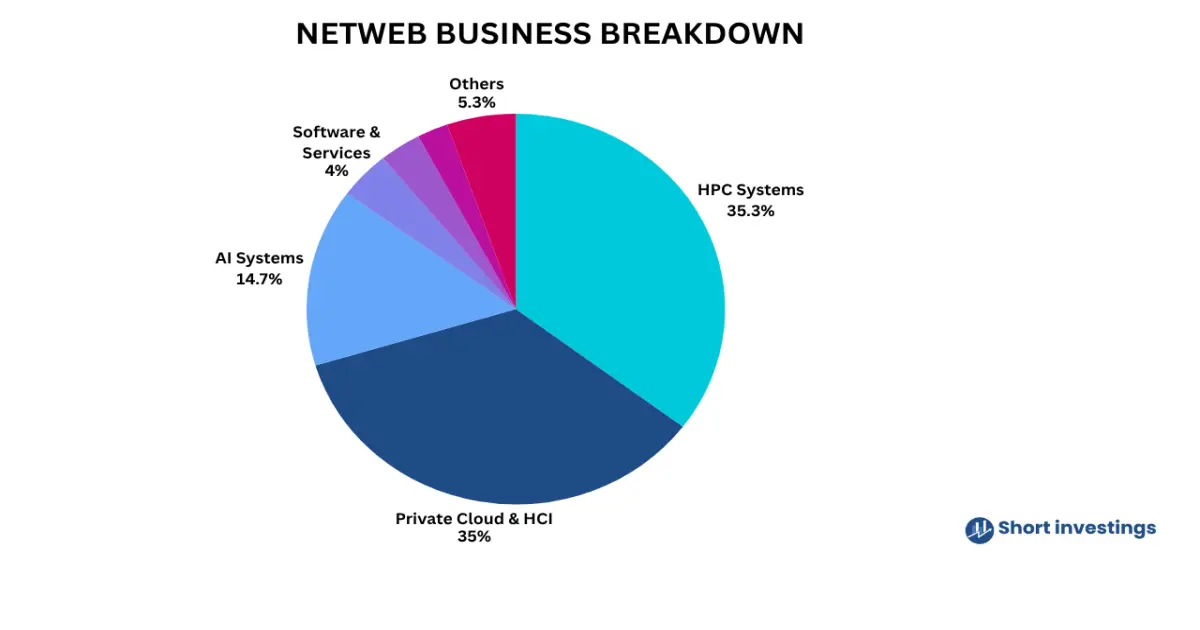

Segment wise breakup

High performance computing business

From a number’s standpoint, the momentum is quite visible. The company reported total revenue of ₹4,055 million in FY2025, growing 54.54% year-on-year. A significant 35% of this revenue is coming directly from the HPC segment, which indicates that this is not a side business—it is a key driver. At the same time, installing 500+ supercomputing systems across the country and having multiple systems featured in the global top 500 list reflects both scale and credibility.

What I find important here is how the company is positioning itself technologically. With its own cluster management capabilities and the ability to scale systems from small nodes to very large clusters, it is not dependent on a single type of deployment. The focus on mixed workload architecture—combining HPC, AI, and data workloads—shows that the company is aligning itself with how computing demand is evolving, especially with AI becoming more central.

At the industry level, the opportunity also looks supportive. The HPC market itself is growing steadily, and Netweb is already present with a strong base of installations. This gives it a natural advantage as demand increases, especially in AI-led workloads and data-intensive applications.

That said, while the growth and positioning are strong, this remains a technology-driven business where continuous innovation and execution will matter. The company has shown good traction so far—both in terms of revenue growth and deployment scale—but sustaining this momentum will depend on how well it keeps up with rapid changes in AI and computing infrastructure.

High-performance storage (HPS)

When you look beyond the headline growth, these segments give a clearer idea of how Netweb is structuring its business for the long term.

The high-performance storage (HPS) segment is a good example of this. The company generated around ₹275 million from this segment in FY2025, with 18.88% YoY growth, contributing about 3% to total revenue. On the surface, the contribution looks small—and even the revenue has come down compared to the previous year—but the underlying capability is quite strong. These systems are designed for high-speed, high-volume data handling, supporting very high IOPS and large-scale throughput.

What stands out to me is that this is not just a basic storage offering. The architecture supports large enterprise workloads, integrates with both private and public cloud environments, and is built with high availability in mind. In simple terms, this segment is more about enabling the broader ecosystem—especially AI and HPC—rather than being a standalone growth driver today. The slowdown in revenue suggests that demand can be uneven in the short term, but the role of storage in data-heavy computing remains critical.

On the other hand, the data centre server segment reflects a more execution-driven side of the business. Netweb has built a wide portfolio here, including dual-processor servers, GPU-based systems, and high-memory configurations. The ability to support up to 6 TB of DDR5 memory and advanced processors shows that the company is targeting performance-intensive use cases, not just standard enterprise demand.

An important layer here is the Tyron ProServe platform. This moves the offering beyond hardware into infrastructure management—giving clients visibility into performance, power usage, system health, and more. This kind of integration improves operational efficiency for customers and makes the offering more sticky over time.

From a balanced perspective, both segments serve different roles. Storage is still in a relatively early phase in terms of revenue contribution and has seen some volatility, but it is strategically important as data workloads grow. The server business, meanwhile, looks more established and directly aligned with current demand in data centres and enterprise IT.

Software and services for hybrid cloud (HCS)

This part of the business—software and services for hybrid cloud (HCS)—is where Netweb’s story starts shifting from hardware to a more complete technology solution.

At a basic level, the company is building its own private cloud software stack to manage complex and data-heavy workloads. Services like application migration, virtual machine migration, and system design show that it is not just selling infrastructure, but helping customers actually use and scale it. This naturally makes the offering stickier and more long-term.

But the real highlight here is the growth.

The segment revenue has moved from ₹176 million in FY2024 to ₹455 million in FY2025, which is a sharp 158.52% year-on-year growth. Over a slightly longer period, the CAGR is also very strong. Even though the contribution to total revenue is still around 4%, the pace at which this segment is scaling clearly stands out.

From my perspective, this kind of growth usually signals that the company is tapping into a new demand cycle rather than just expanding an existing one.

Another important piece is the technological positioning. The solutions are built to support not just enterprise IT, but also edge computing, 5G environments, and large-scale cloud deployments. When combined with Netweb’s own hardware stack—servers, storage, and HPC—it creates a more integrated ecosystem rather than isolated products.

The big data capability is also worth noting. Integration with its own systems like Tyrone CAMARERO and cluster management tools shows that the company is trying to control both compute and data layers. This is important because in AI and data-driven environments, performance depends on how well compute, storage, and software work together.

Client deployments in places like NMDC Data Centre and Graviton further indicate that these solutions are not just theoretical—they are already being used in real, large-scale environments.

That said, taking a balanced view, the segment is still relatively small in terms of overall contribution. At 4%, it is not yet a core revenue driver like HPC. Also, such high growth rates can be partly due to a lower base, so sustaining this pace over the long term will be something to watch.

Cloud and hyperconverged infrastructure (HCI)

This segment—private cloud and hyperconverged infrastructure (HCI)—looks like one of the most important pieces in Netweb’s overall business.

In simple terms, the company is combining compute, storage, and networking into a single integrated solution. Instead of clients managing separate systems, everything is brought together in one platform. This makes it easier for enterprises to run private and hybrid cloud environments, especially when workloads are becoming more complex and data-heavy.

What stands out here is the scale and contribution. The segment generated around ₹4,027 million in FY2025, with a strong 51.16% year-on-year growth, and contributes nearly 35% of total revenue. That makes it one of the largest revenue drivers for the company today—not just a supporting segment.

From a business perspective, this also shows good adoption. The company has already completed more than 50 private cloud and HCI deployments, which indicates that these solutions are not just theoretical—they are being actively used by enterprises.

I see this segment as a bridge between Netweb’s hardware strength and its growing software capabilities. It connects servers, storage, and cloud management into one offering, which is exactly what enterprises are looking for as they move towards hybrid cloud setups.

At the same time, taking a balanced view, this is also a competitive space and requires continuous execution. Growth is strong right now, but maintaining this pace will depend on how well the company keeps delivering integrated and reliable solutions at scale.

Overall, this segment feels like a core pillar of the business today—not only contributing significantly to revenue but also strengthening Netweb’s position as a full-stack infrastructure provider.

AI Systems & Workstations

This part of Netweb’s business ties everything together—it shows how the company is moving from infrastructure to actually powering next-generation tech use cases.

The AI systems and enterprise workstations segment is where this shift becomes very clear. The company is building systems designed for advanced applications like machine learning, generative AI, and engineering simulations. These are not standard computing needs—these are high-performance, specialised workloads where both hardware and software integration matter.

From a numbers perspective, the traction is already visible. The segment generated around ₹1,694 million in FY2025, growing 112.02% year-on-year, and now contributes about 14.8% of total revenue. That’s a meaningful share, especially considering how quickly it has scaled.

What stands out to me is that this is not just demand-driven growth—it’s also capability-driven. The company has already deployed over 5,000+ GPU/accelerator-based systems, which indicates real adoption on the ground. At the same time, the launch of platforms like Skylus AI shows an effort to simplify how AI infrastructure is deployed and managed, rather than just supplying hardware.

From a broader view, this segment sits right at the intersection of all Netweb’s strengths—HPC, storage, servers, and now software. That’s important because AI workloads require a full-stack approach, not isolated products.

At the same time, taking a balanced view, this is still a fast-evolving space. Growth is strong right now, but it is also dependent on how quickly AI adoption continues and how well the company keeps up with technological changes. Competition and continuous innovation will play a big role here.

Key Constraints to business – NVIDIA chips allocation

It’s easy to get carried away with the growth numbers and positioning, but there are a few areas where the story needs a more cautious lens.

One key point is the dependence on NVIDIA-led ecosystem. A large part of Netweb’s AI and HPC growth is clearly tied to GPU-based systems and advanced computing workloads. While this is a strong tailwind today, it also means a significant portion of the opportunity is indirectly dependent on NVIDIA’s supply, roadmap, and ecosystem control. If GPU availability becomes tight or allocation remains restricted, it can directly limit how much Netweb can actually deliver—no matter how strong the demand is.

| Segment | FY22 (₹M) | FY23 (₹M) | FY24 (₹M) | FY25 (₹M) | CAGR | FY25 Share |

|---|---|---|---|---|---|---|

| High-Performance Computing | 1,030 | 1,728 | 2,624 | 4,055 | 57.9% | 35% |

| Private Cloud & HCI | 479 | 1,461 | 2,644 | 4,027 | 103.4% | 35% |

| AI Systems & Enterprise Workstations | 243 | 309 | 799 | 1,694 | 91.0% | 15% |

| Data Centre Servers | 241 | 283 | 337 | 373 | 15.7% | 3% |

| High-Performance Storage (HPS) | 217 | 308 | 339 | 275 | 8.2% | 2% |

| Software & Services for HCS | 69 | 95 | 176 | 455 | 87.6% | 4% |

| Total | 2,279 | 4,184 | 6,919 | 10,879 | — | 100% |

This connects to the second concern—server and AI system scalability is not fully in the company’s control. Even though Netweb designs and integrates systems, the critical components (like GPUs and high-end chips) are externally sourced. So, growth in segments like AI systems (which are currently growing above 100%) may face practical constraints if supply doesn’t match demand.

Another point is the uneven contribution across segments. While AI and HPC are driving strong growth, other segments like storage are still small (around 3%) and have even seen some slowdown in revenue. Similarly, the hybrid cloud/software segment, despite high growth, contributes only about 4%. This means the business is still heavily dependent on a few core segments rather than having balanced growth across all verticals.

There’s also the factor of high growth coming from a relatively lower base in newer segments. For example, the 150%+ growth in the HCS segment looks impressive, but the absolute contribution is still limited. Sustaining such high growth rates as the base increases will be more challenging.

From a customer perspective, while diversification between government and non-government is balanced, a large part of the demand still comes from institutional and enterprise projects. These can sometimes be lumpy in nature, which may impact consistency in revenue flow.

So, while the company is clearly moving in the right direction—especially in AI, HPC, and integrated infrastructure—the growth story is not without dependencies. A lot of the execution will depend on external supply chains, especially GPUs, and how well the company can scale its smaller segments into meaningful contributors.

Overall, Netweb has built a strong presence across HPC, AI, servers, storage, and cloud, positioning itself well in a high-growth computing ecosystem. Its ability to serve multiple sectors and deliver integrated solutions adds depth to the business. A key strength remains its close alignment with the NVIDIA ecosystem, which is playing an important role in scaling its AI and high-performance computing capabilities. This combination of strong market presence and strategic partnership puts the company in a favorable position as demand for advanced computing continues to grow.

1 thought on “Netweb Technologies Business Model: Segment-Wise Breakdown”